2026年シーズンを迎えるアメリカにおいて、静かな予測と壊滅的な上陸の差は、依然として1つの嵐だけです。ここでは、保険会社、MGA、TPAのクレームリーダーが、受動的な対応から脱却し、主導的立場を築く方法を紹介します。.

脅威

「静かな」シーズンは安全なシーズンではない

NOAA 2026年公式見通し, released May 21, forecasts a below-normal Atlantic hurricane season: 8 to 14 named storms, indicating 55% probability of below-normal activity. Many insurers will be breathing a sigh of relief.

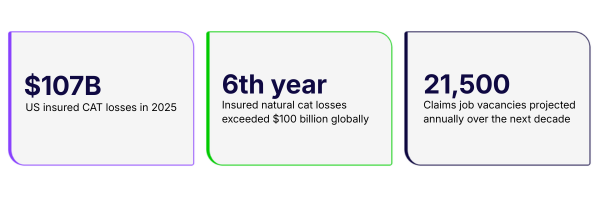

すべきではありません。NOAA の長官が述べたように、「1 つの嵐で 1 年のシーズンが非常に悪くなることはあります。」2022 年の平年以下のシーズン中に、ハリケーン イアンはフロリダを壊滅させました。2025 年に発生し、 $ 世界の保険金支払額は1070億 大西洋盆地の予報とは関係ありませんでした。米国の航空会社にとって現在最も懸念される頻度の高い事象である、ひょう、強風、竜巻などの激しい対流性嵐は、公式の季節暦を待たずに発生します。.

“「80%による手動受付で1日200件の保険金請求を処理している保険金請求業務は、品質の低下を招くか、あるいは生産性を発揮するまでに6~8週間を要する臨時査定員を採用しない限り、1日2,000件の処理規模に拡大することはできない。」”

ロイ・アミール、, CEO、Sprout.ai

数学は容赦ない。そして2026年に向かう構造的条件は、それを改善するどころか悪化させている。.

なぜこれが悪化しているのか

毎年CATの対応を難しくしている3つの収束する要因

2026年に向けての業界分析によると、静かな季節的予測では解決できない、同じような複合的な圧力のクラスターが継続している。.

損失の深刻度は、発生頻度に関係なく上昇し続けています。

LexisNexis 米国の住宅トレンドレポート, 2025年後半に発表された報告書によると、2023年から2024年にかけて、全危険種別における損害の深刻度は9%増加し(7年間で最高値)、損害コストは2019年の水準を50%近く上回った。 大災害による保険金請求件数は全請求件数の42%を占めたが、総損害額の64%を占めた。2024年には、風災による損害の深刻度だけでも23%以上急増した。気候変動による災害の激化により、以前は管理可能だった事象のコスト構造さえも変化しつつある。.

二次的な災害は、ますます運用上の問題となっています

Insurers surveyed during summer 2025 identified severe convective storms (SCS), not named hurricanes, as their top concern. These events generate high-frequency, geographically dispersed claims that arrive in concentrated bursts, testing the surge capacity of teams that were sized for average volume. A carrier absorbing 5,000 SCS claims across a three-state outbreak in 72 hours faces a different intake and decisioning challenge than a single large hurricane event.

人材パイプラインは壊れている

2026年末までに、米国では2021年以降、推定40万人の保険専門家が退職すると見られています。 労働統計局 (BLS)のデータによると、BLSは今後10年間で年間約21,500件の保険金請求関連の求人があるとの見通しを示している。 金融・保険業界の雇用数は、2022年のピーク時より27%下回っている。従来、自然災害(CAT)発生時の業界の安全弁として機能してきた緊急増員体制は、現在では確実に確保できず、また、臨時で採用された損害査定員が十分な生産性を発揮できるようになるまでには6~8週間を要する。.

複合リスク

請求コストは一般インフレよりも速く上昇しています。頻度と重大性が同時に増加しています。経験豊富な査定人の能力は低下しています。これら3つの力は、まさにボリュームが急増する瞬間に収束しますが、季節的なものではありません。構造的なものです。.

保険会社とMGA(マネージド・インシュアランス・ジェネラル・エージェント)は、急増イベント中に発生する損失率の変動性と高い損害査定費用(LAE)を、それぞれを定義する問題点と捉えています。課題の根源は同じですが、ビジネスモデルによってその結果は異なります。.

セグメント別運用実績

貴社にとってCATシーズンの圧力はどのようなものですか

問題の本質は、請求チェーンのどこにいるかによって異なります。.

| 保険会社 大規模におけるボリューム、一貫性、および規制上の防御可能性 Carriers optimize for combined ratio and regulatory defensibility. During a CAT event, every coverage decision made under surge conditions, by any adjuster, on any system, needs to be explainable and defensible across all states. Social inflation is amplifying the stakes: According to スイス・リー・シグマ, 、過去10年間で米国の損害賠償請求件数は57%増加した。規制当局は、まさにプレッシャーが最も高まっているこの時期に、公正な保険金支払いの取り扱いに対する監視を強化している。リスクは単に「漏れ」だけにとどまらず、大規模な不整合が生じ、同時に発生する数千件の保険金請求によってその影響が相乗的に拡大することにある。. | MGAS 損失比率エクスポージャーは、キャパシティの関係です MGAs optimize for loss ratio performance and capacity confidence. CAT season is a trust test with capacity partners: a loss ratio that drifts during a surge event affects whether carriers and reinsurers renew, reprice, or withdraw authority. Lean teams and limited adjusting capacity make surge management an existential question. MGAs operating through TPAs face an additional challenge: outcomes are partly outside their direct control, and visibility is only as good as their data from delegated partners. |

| TPAS SLAは契約であり、サージは交渉決裂の要因になり得ます TPAs win mandates on capability and retain them on performance. CAT events are the moment when both are simultaneously visible, to every client, across every SLA metric. A TPA that can demonstrate surge-resilient performance, consistent decisioning across a diverse client portfolio, and audit-ready reporting through a major event has a durable competitive advantage. | 共有された問題 Manual processes don’t scale, anywhere in the chain Regardless of business type, CAT events expose the same underlying fragility: claims operations built around manual document review and siloed systems cannot absorb a sudden order-of-magnitude increase in volume without degradation. 30–50% of adjuster time is already spent reading and keying data under normal conditions. The question isn’t whether to automate the routine; it’s whether the intelligence layer is in place before the event arrives. |

良い準備とは

事後対応からオペレーショナル・レジリエンスへの移行

クロフォード&カンパニーの業界分析 2026年 クレーム動向レポート クレームリーダーが急増への耐久性を構築するための5つの優先事項を特定する.

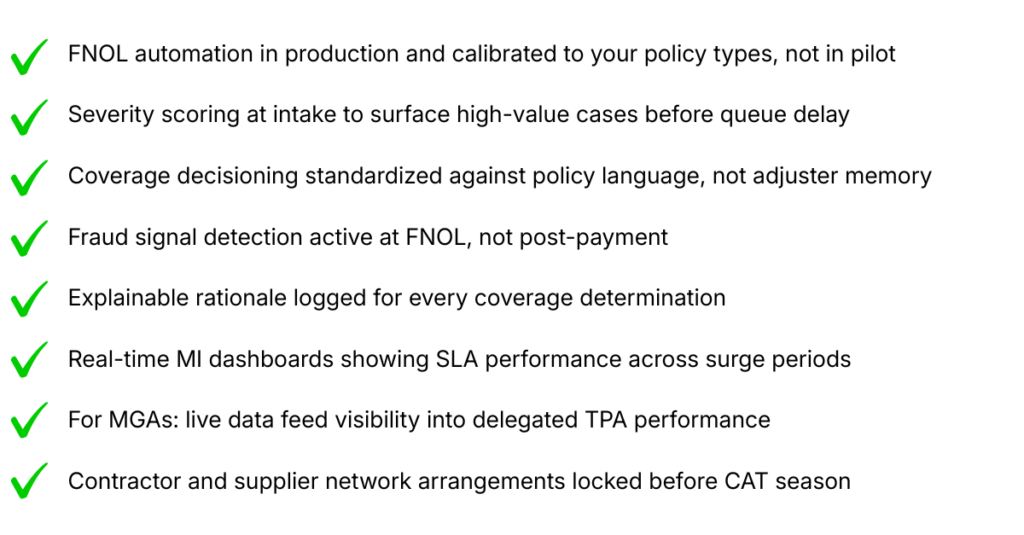

- イベント開催前に入力作業を自動化し、開催中は行わないようにする。. FNOL automation is a mature capability in 2026. The global AI-in-claims market is growing at 23.5% CAGR, driven by exactly this use case: surge-volume intake that doesn’t degrade with scale. AI-powered intake must be in production and calibrated to your policy types before an event, not deployed reactively. Top performing insurers eliminate data noise and settle simple claims before they reach adjusters.

- ルーティングだけでなく、トリアージにもインテリジェンスを組み込む。. Routing claims to the right handler is necessary but insufficient. AI-enabled severity scoring and completeness checking at intake means high-value, high-risk, and legally sensitive claims surface immediately, rather than emerging from a queue days later when decisions have already drifted. Supported, augmented adjusters drive efficiency, consistency, and satisfaction; this is what “good” looks like for both carriers and MGAs.

- 調整者のばらつきによる漏洩を防ぐため、カバレッジの決定を標準化してください。. Industry estimates of claims leakage run at 5–10% of total claims costs under normal conditions. Under surge, with inexperienced temporary adjusters and compressed timelines, leakage climbs. Policy-aware AI that reads each claim against the relevant coverage, clause by clause, creates consistent, defensible decisions that don’t depend on which adjuster opens the file. For carriers, this is LAE and combined ratio. For MGAs, this is the loss ratio their capacity partners monitor.

- 規制当局の審査に耐えうる監査証跡を作成する. Every coverage determination made during a surge event needs to be traceable, explainable, and documented across all states. AI-generated decision rationales create a portable audit trail. For TPAs, this is also the client-reportable evidence base that demonstrates SLA adherence and claims discipline in concrete, measurable terms.

- MGAsおよびTPAsにとって、委任されたクレームに対するリアルタイムのデータ可視性は、選択肢ではありません。. The delegated claims model creates structural information asymmetry. In a CAT event, real-time management information on TPA performance (SLA adherence, decision consistency, complaint signals) is the operational infrastructure that lets an MGA demonstrate disciplined claims handling to capacity partners when it matters most. Transparent, defensible claims decisions are the credential that determines whether capacity partners renew.

CATシーズン準備チェックリスト

“Even a ‘below-normal’ forecast should be read as breathing space to strengthen portfolios and client preparedness, not as an all-clear.” Insurance Business, May 2026

SPROUT.AIの活用方法

Sprout.aiがCATシーズン請求インテリジェンスにユニークなポジションにある理由

The capabilities described in this article – automated intake, policy-aware decisioning, explainable AI, real-time MI – are live, in production, processing millions of claims annually across carriers, MGAs, and TPAs on three continents.

| ザ・テック CATイベント中に大量に届く、PDF、写真、メール、FNOLフォーム、修理見積もりといった、複雑で多様な形式の文書に対応する、専用の文書インテリジェンス。. 保険業界に特化したデータ抽出機能で、本番環境でのOCR精度は97%を超えています。汎用OCRを後付けで適用したものではありません。. 保険業界に特化したデータ抽出機能で、本番環境でのOCR精度は97%を超えています。汎用OCRを後付けで適用したものではありません。. | 知性 ポリシーを認識するAIは、各請求を特定のポリシーに対して読み込み、条項ごとに制限と免責事項を確認し、完全な理由付けとともに説明可能な推奨事項を生成します。. 実稼働環境において、F1のスコアは96%を上回っています。. 67-95% STPの処理速度は、タイプや複雑さによって異なります。. すべての調整者、すべてのサージ条件で一貫しており、ボリュームが増えても決定が低下しません。. | 約束 契約された成果、ベンダーの予測ではない。書面で約束された精度目標。. 通常の数週間で実装できるため、数ヶ月ではなく、請求業務はすぐに開始でき、カタストロフシーズンのピーク前には稼働できます。. データフライホイールは時間とともに複利で増加します。処理されたすべての請求が、次のモデルを改善します。. |

For carriers, the business case ROI is combined ratio.

For MGAs, it is the capacity partner confidence that comes from demonstrable claims discipline.

For TPAs, it is the SLA performance and client-reportable audit trail that wins mandates and retains them.

インテリジェンスレイヤーは同じです。ビジネスケースは、チェーンのどこに位置するかによって異なります。.

請求業務の限界を露呈させるために、次のCATイベントを待たないでください。.

見て Sprout.ai helps carriers, MGAs, and TPAs automate intake, standardize coverage decisions, and scale claims handling without compromising accuracy or compliance.