As the US heads into the 2026 season, the gap between a quiet forecast and a catastrophic landfall is still just one storm. Here’s how claims leaders across carriers, MGAs, and TPAs can stop reacting and start leading.

THE THREAT

A “quieter” season is not a safe season

The NOAA official 2026 outlook, released May 21, forecasts a below-normal Atlantic hurricane season: 8 to 14 named storms, indicating 55% probability of below-normal activity. Many insurers will be breathing a sigh of relief.

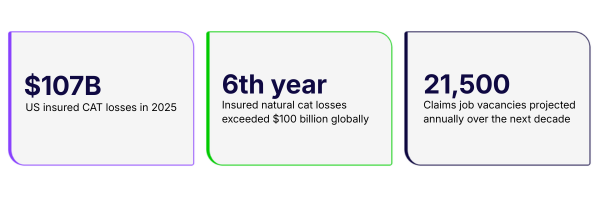

They shouldn’t. As NOAA’s own director put it: “It only takes one storm to make for a very bad season.” Hurricane Ian devastated Florida during a below-normal 2022 season. The LA wildfires that opened 2025 and drove $107 billion in global insured losses had nothing to do with the Atlantic basin forecast. Severe convective storms (the hail, wind, and tornado outbreaks that now represent the highest-frequency concern for US carriers) don’t wait for the official seasonal calendar.

“A claims operation that handles 200 claims per day with 80% manual intake cannot scale to 2,000 claims per day without either quality degradation or hiring temporary adjusters who take 6–8 weeks to reach productivity.”

Roi Amir, CEO, Sprout.ai

The math is unforgiving. And the structural conditions going into 2026 make it worse, not better.

WHY THIS IS GETTING WORSE

Three converging forces that make CAT response harder every year

Industry analysis going into 2026 shows the same cluster of compounding pressures, none of which a quiet seasonal forecast resolves.

Loss severity keeps rising, independent of frequency

The LexisNexis US Home Trends Report, released in late 2025, found that all-peril severity increased 9% between 2023 and 2024 (the highest in seven years), while loss costs ran nearly 50% above 2019 levels. Catastrophe claims represented 42% of all claims in number, but 64% of total losses. Wind severity alone surged over 23% in 2024. Climate-driven intensity is changing the cost profile of events that would previously have been manageable.

Secondary perils are increasingly the operational problem

Insurers surveyed during summer 2025 identified severe convective storms (SCS), not named hurricanes, as their top concern. These events generate high-frequency, geographically dispersed claims that arrive in concentrated bursts, testing the surge capacity of teams that were sized for average volume. A carrier absorbing 5,000 SCS claims across a three-state outbreak in 72 hours faces a different intake and decisioning challenge than a single large hurricane event.

The talent pipeline is broken

By the end of 2026, an estimated 400,000 insurance professionals will have retired in the US since 2021, per Bureau of Labor Statistics (BLS) data. The BLS projects roughly 21,500 claims job vacancies annually over the next decade. Finance and insurance hiring sits 27% below its 2022 peak. Surge staffing, historically the industry’s safety valve for CAT events, is not reliably available, and temporary adjusters take 6–8 weeks to reach competent productivity.

The compounding risk

Claims costs are rising faster than general inflation. Frequency and severity are increasing together. Experienced adjuster capacity is declining. These three forces converge precisely at the moments when volume spikes, and they are not seasonal. They are structural.

Both carriers and MGAs see loss ratio volatility and high Loss Adjustment Expense (LAE) as their defining pain points during surge events; the challenge is identical in origin, but the consequences differ by business model.

OPERATIONAL REALITY BY SEGMENT

What CAT season pressure looks like for your organization

The nature of the problem differs depending on where you sit in the claims chain.

| INSURANCE CARRIERS Volume, consistency, and regulatory defensibility at scale Carriers optimize for combined ratio and regulatory defensibility. During a CAT event, every coverage decision made under surge conditions, by any adjuster, on any system, needs to be explainable and defensible across all states. Social inflation is amplifying the stakes: According to Swiss Re Sigma, US liability claims grew 57% over the past decade. Regulators are intensifying scrutiny of fair claims handling precisely when the pressure is highest. The risk isn’t just leakage; it’s inconsistency at scale, compounding across thousands of simultaneous claims. | MGAS Loss ratio exposure is the capacity relationship MGAs optimize for loss ratio performance and capacity confidence. CAT season is a trust test with capacity partners: a loss ratio that drifts during a surge event affects whether carriers and reinsurers renew, reprice, or withdraw authority. Lean teams and limited adjusting capacity make surge management an existential question. MGAs operating through TPAs face an additional challenge: outcomes are partly outside their direct control, and visibility is only as good as their data from delegated partners. |

| TPAS SLAs are the contract and surge can be a deal breaker TPAs win mandates on capability and retain them on performance. CAT events are the moment when both are simultaneously visible, to every client, across every SLA metric. A TPA that can demonstrate surge-resilient performance, consistent decisioning across a diverse client portfolio, and audit-ready reporting through a major event has a durable competitive advantage. | THE SHARED PROBLEM Manual processes don’t scale, anywhere in the chain Regardless of business type, CAT events expose the same underlying fragility: claims operations built around manual document review and siloed systems cannot absorb a sudden order-of-magnitude increase in volume without degradation. 30–50% of adjuster time is already spent reading and keying data under normal conditions. The question isn’t whether to automate the routine; it’s whether the intelligence layer is in place before the event arrives. |

WHAT GOOD PREPARATION LOOKS LIKE

Moving from reactive response to operational resilience

Industry analysis from Crawford & Company’s 2026 claims trends report identifies five priorities for claims leaders building surge resilience.

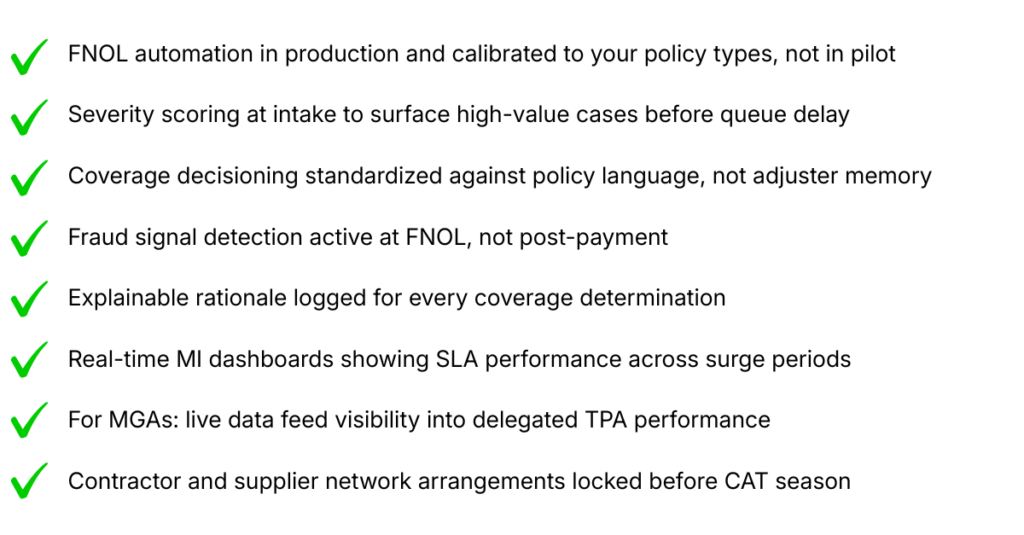

- Automate intake before the event, not during it. FNOL automation is a mature capability in 2026. The global AI-in-claims market is growing at 23.5% CAGR, driven by exactly this use case: surge-volume intake that doesn’t degrade with scale. AI-powered intake must be in production and calibrated to your policy types before an event, not deployed reactively. Top performing insurers eliminate data noise and settle simple claims before they reach adjusters.

- Build intelligence into triage, not just routing. Routing claims to the right handler is necessary but insufficient. AI-enabled severity scoring and completeness checking at intake means high-value, high-risk, and legally sensitive claims surface immediately, rather than emerging from a queue days later when decisions have already drifted. Supported, augmented adjusters drive efficiency, consistency, and satisfaction; this is what “good” looks like for both carriers and MGAs.

- Standardize coverage decisions before adjuster variability creates leakage. Industry estimates of claims leakage run at 5–10% of total claims costs under normal conditions. Under surge, with inexperienced temporary adjusters and compressed timelines, leakage climbs. Policy-aware AI that reads each claim against the relevant coverage, clause by clause, creates consistent, defensible decisions that don’t depend on which adjuster opens the file. For carriers, this is LAE and combined ratio. For MGAs, this is the loss ratio their capacity partners monitor.

- Create audit trails that survive regulatory scrutiny. Every coverage determination made during a surge event needs to be traceable, explainable, and documented across all states. AI-generated decision rationales create a portable audit trail. For TPAs, this is also the client-reportable evidence base that demonstrates SLA adherence and claims discipline in concrete, measurable terms.

- For MGAs and TPAs: real-time data visibility into delegated claims is not optional. The delegated claims model creates structural information asymmetry. In a CAT event, real-time management information on TPA performance (SLA adherence, decision consistency, complaint signals) is the operational infrastructure that lets an MGA demonstrate disciplined claims handling to capacity partners when it matters most. Transparent, defensible claims decisions are the credential that determines whether capacity partners renew.

CAT season readiness checklist

“Even a ‘below-normal’ forecast should be read as breathing space to strengthen portfolios and client preparedness, not as an all-clear.” Insurance Business, May 2026

HOW SPROUT.AI HELPS

Why Sprout.ai is uniquely positioned for CAT season claims intelligence

The capabilities described in this article – automated intake, policy-aware decisioning, explainable AI, real-time MI – are live, in production, processing millions of claims annually across carriers, MGAs, and TPAs on three continents.

| THE TECH Purpose-built document intelligence for the messy, multi-format documents that arrive in volume during a CAT event (PDFs, photos, emails, FNOL forms, repair estimates). Insurance-native extraction, with OCR accuracy above 97% in production deployments. Not retrofitted generic OCR. Insurance-native extraction, with OCR accuracy above 97% in production deployments. Not retrofitted generic OCR. | THE INTELLIGENCE Policy-aware AI reads each claim against the specific policy and confirms limits and excesses, clause by clause, producing an explainable recommendation with full rationale. Coverage F1 scores above 96% in production. 67-95% STP rates achieved, depending on type and complexity. Consistent across every adjuster and every surge condition; decisions don’t degrade under volume. | THE COMMITMENT Contracted outcomes, not vendor projections. Accuracy targets committed in writing. Typical implementation measured in weeks, not quarters, meaning a claims operation that acts now can be live before peak CAT season. A data flywheel compounds over time: every claim processed improves the models for the next. |

For carriers, the business case ROI is combined ratio.

For MGAs, it is the capacity partner confidence that comes from demonstrable claims discipline.

For TPAs, it is the SLA performance and client-reportable audit trail that wins mandates and retains them.

The intelligence layer is the same. The business case is specific to where you sit in the chain.

Don’t wait for the next CAT event to expose the limits of your claims operation.

See how Sprout.ai helps carriers, MGAs, and TPAs automate intake, standardize coverage decisions, and scale claims handling without compromising accuracy or compliance.